A “Private Equity” Mini-Portfolio That Yields 10%-Plus

Private equity (PE) is a rich guy and gal favorite. PE firms find deals and deliver outsized dividends.

They don’t like dealing with common folk. So, PE shops typically set a minimum of a few hundred thousand dollars or so to invest.

But we contrarians have a better way! By tapping BDCs—or business development companies—we can toss as little as $20 into a PE payer.

Better yet, we can secure yields between 8.5% and 13.1%. We’ll discuss three examples today. Including one that is trading below book value!

If you’ve never heard of business development companies (BDCs), you’re not alone. There are only a few dozen publicly traded BDCs, and even the largest one would be a minnow in the S&P 500.

BDCs, which were created by Congress a few decades ago, provide much-needed capital to companies that you and I could never invest in otherwise. Each BDC usually invests in dozens to hundreds of these companies at any given time, making them de facto private equity specialists.

But what I love most about business development companies are their gargantuan dividends—dividends that are required by their very structure.

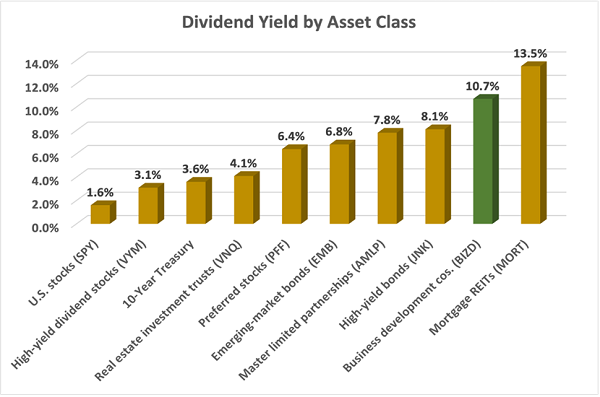

Like REITs, BDCs must pay out at least 90% of their taxable income as dividends, though they have much higher horsepower as a group than REITs—and most other asset classes, for that matter:

On Yield Alone, It’s Hard to Beat BDCs

But super-powered double-digit yields are rarely super-safe as well. In fact, BDCs as a group can be a dog, which is why you should avoid investing in them through diversified funds. Instead, you need to find the few picks of the litter—and avoid the rest at all costs.

Here are three—yielding an astounding 8.5% to 13.1%—that exemplify BDCs’ highs and lows.

Main Street Capital (MAIN)

Dividend Yield: 8.5%

Main Street Capital (MAIN) is as much of a blue-chip stock as the BDC industry has.

This $3 billion business development company provides debt and equity capital solutions to lower-middle-market companies, and debt financing (primarily floating-rate first lien senior secured debt) to middle-market firms.

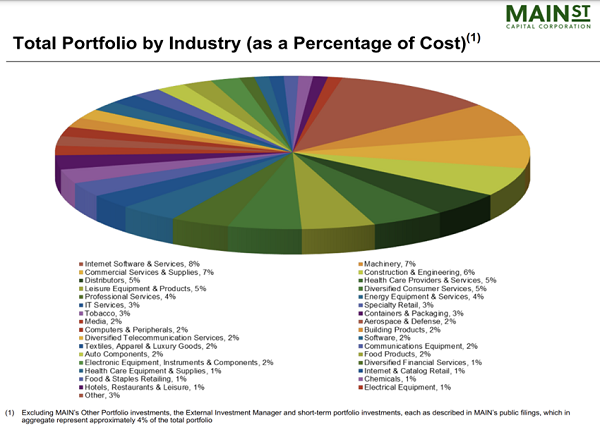

MAIN’s typical target company generates annual revenues of between $10 million and $150 million, and roughly $3 million to $20 million in EBITDA. Currently, its portfolio is made up of 194 companies, with the largest one representing just 3.4% of total investment income. And from an industry perspective, you couldn’t ask for more diversification:

Included in these companies is MSC Adviser—the company’s external investment advisor, which has been steadily contributing more to the BDC’s results over the past few years.

Main Street is one of the best operators in the space, and its Q4 2022 merely added to its track record. Net investment income (NII) per share soared past estimates, return on equity was north of 20%, and distributable NII per share was 56% more than what it needed to fund its monthly dividends.

Speaking of the dividend: Not only is MAIN a monthly payer, but in a nod to fiscal responsibility, it also utilizes quarterly special distributions that ebb and flow as income allows. As a result, its most recent special distribution was 17.5 cents—75% better than its past two 10-cent top-ups. The yield on its monthly is 6.8% right now; the special annualizes out to another 1.7%.

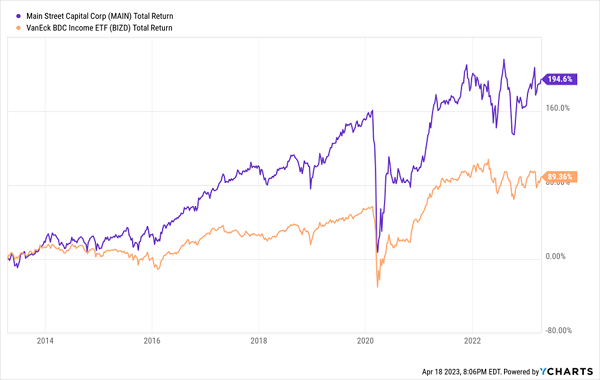

MAIN seemingly always flies one massive red flag, however: its valuation. It’s the most expensive BDC on the market, and by a comfortable margin, at 1.5 times its net asset value. Obviously, as you can see, MAIN has been able to outperform long-term despite this, but the valuation has seemingly put a cap on shares over the past few years.

Main Street Capital: Growth at an Unreasonable Price

Gladstone Capital (GLAD)

Dividend Yield: 10.0%

A more reasonably priced BDC is Gladstone Capital (GLAD), which invests in lower middle market businesses.

Gladstone Capital is just one of several companies in the Gladstone “family” of investment acronyms—a group that also includes fellow BDC Gladstone Investment Corporation (GAIN), as well as real estate investment trusts (REITs) Gladstone Land (LAND) and Gladstone Commercial Corporation (GOOD).

This particular Gladstone uses everything from revolving loans and senior term loans to unitranche loans and even minority equity to provide capital to companies with $20 million to $150 million in annual revenues, $3 million to $25 million in EBITDA, limited market and/or technology risk, and the potential to expand cash flow.

Gladstone Capital features a much smaller portfolio than Main Street, at just 50 companies spread across 15 different industries. But overall, it has a defensive stance, with healthcare, aerospace, and education among its largest industry concentrations.

Portfolio companies range from antenna manufacturer Antenna Research Associates to residential repair specialist Fix-It Group to artisanal ice cream company Salt & Straw.

GLAD’s investments are predominantly debt-based, and 90% of those investments are floating-rate in nature, so higher interest rates have been more help than harm. Meanwhile, Gladstone offers a sturdy balance sheet, and a generous management team that has shared the wealth via four hikes to the monthly dividend since the start of 2022.

At 1.05 times NAV, Gladstone’s shares aren’t exactly a steal. But they’re just a little more than fairly valued, and at the lower end of their historical range.

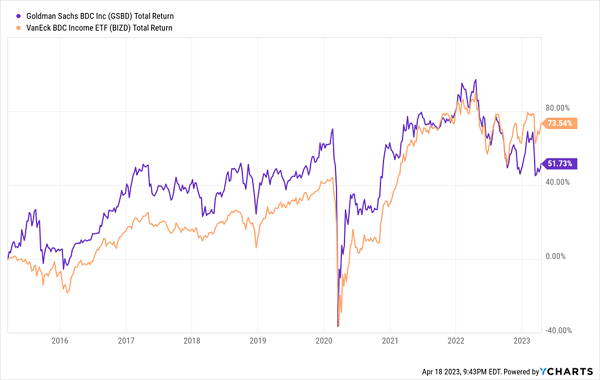

Goldman Sachs BDC (GSBD)

Dividend Yield: 13.1%

It’s hard to think of many BDCs that have an advantage quite like Goldman Sachs BDC (GSBD):

“We are able to draw upon the vast resources of Goldman Sachs to assist in the evaluation of potential investment opportunities and to provide a range of value-added services to our portfolio companies.”

And yet …

Goldman Sachs’ Wall Street Pedigree Has Lost Its Edge

It’s hard to ignore that screaming 13% yield, though, and a slight discount to NAV, so let’s see if GSBD is just waiting to pounce.

This band of some of Wall Street’s finest typically invests anywhere between $25 million to $75 million in U.S. middle market companies with EBITDA of between $5 million and $75 million annually, and it’s happy to source partners for bigger deals.

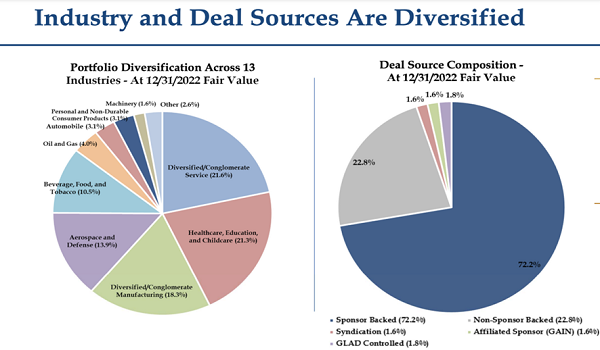

GSBD’s current portfolio includes 134 companies, spread across industries including software, financial services, healthcare and professional services. The firm’s investments are overwhelmingly loaded up on first- and second-lien debt, which have extremely low default probability.

But there are some noteworthy cracks. Debt-to-equity remains above company targets. Non-accruals (typically, companies that haven’t paid in 90 days) were at 2.1% at amortized cost, including two new portfolio companies placed on non-accrual last quarter. Growth has been intermittent at best over the past few years. And dividends do all of the talking—a five-year total return of just less than 20% belies a nearly 30% share-price decline in the same time.

Give Me 4 Minutes, I’ll 4X Your Retirement Income

If we want a cozy, comfortable retirement without bleeding your nest egg dry, we need to be able to plan around our income with laser precision—and BDCs that are either wildly overpriced or perennial underperformers don’t exactly scream “long-term dividend security.”

Fortunately, there are plenty of safe harbors in our “Perfect Income” portfolio—and you can enjoy their security and sky-high dividends, too.

The perfect dividend retirement stocks have several things in common:

- They pay you consistently, predictably and reliably.

- They’re built to survive—even thrive—in market crashes.

- They deliver double-digit returns, with safe, secure investments.

- They take just a few minutes every month to “manage.”

- They DON’T involve day trading, buying on margin or any other risky strategy.

- They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Take control of your financial legacy today. Click here for my newly updated briefing on the Perfect Income Portfolio!

This post originally appeared at Contrarian Outlook.

Category: Dividend Yield