No Rate Worries Here, Just Tax-Advantaged Yields Up to 7.8%

Image by Pixabay

Does a rising 10-year Treasury yield mean we should move on from municipal (muni) bonds? We’ll talk muni strategy in a moment. First, let’s pay homage to these tax-efficient payers.

Munis are superior to Treasuries two ways. First, they pay more. Even with the 10-year rate popping above 1.6% earlier this week, we can double or triple our dividends with munis. The iShares National Muni Bond ETF (MUB), for example, yields 2.1%, which is 30%+ better than the still-chintzy T-Bill.

Plus, munis have tax benefits. MUB is an easy-to-buy vehicle with a tax-advantaged payout that is higher than its stated 2.1% yield.

For investors looking to save on taxes, MUB is a popular option. Unfortunately it is marketed as such to investors who don’t know any better. (Many ETFs tend to be convenient tickers that underperform smarter alternatives in the income world.)

We careful contrarians prefer to purchase Nuveen’s AMT-Free Municipal Credit Income Fund (NVG), which pays 4.9%—over three times the skinflint Treasury. NVG is a closed-end fund (CEF), which means it is actively managed. Financial talking heads have turned “active management” into a dirty word in recent years, but in the muni world, “active” is a big advantage.

The muni bond market is a throwback to a simpler time. Many deals are still brokered on good old-fashioned landlines. Nuveen gets the first phone call when muni bonds are issued, and NVG’s superior returns and yield reflect this advantage.

Both MUB and NVG are exempt from federal taxes. For top income bracket ballers, this elevates a 4.9% yield to 7.8%. Who wants a Treasury now?

NVG pays us a neat, tax-efficient $0.068 on the second week of the month. Every month. But we don’t want the value of the fund’s bonds to decline as it’s dishing us this monthly dividend. Heck, we don’t want its price to decline at all.

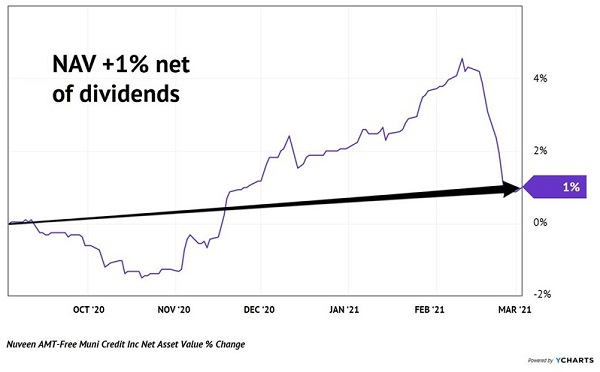

Fortunately, NVG says “no problem.” Over the last six months, NVG’s net asset value (NAV)—the market price of the muni bonds it owns net of debt—has appreciated by 1%. Remember, this is also net of dividends paid, so this modest appreciation is perfect. All we ask from NVG (and its NAV) is that it stays steady over time while it pays us monthly.

NVG’s Muni Portfolio, Net of Dividends Paid (6 Months)

True, the path taken to the 1% is a bit concerning. On the far-right we do see that NVG has shed some NAV in recent weeks as the 10-year rate has spiked. Let’s take a closer look at this relationship:

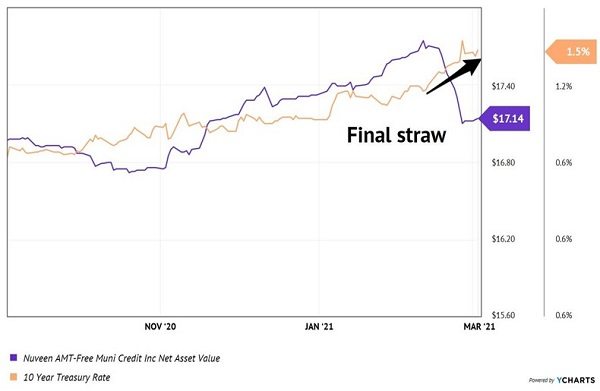

The 10-Year Rate Move From 1.2% to 1.5%+ Did It

This chart reminds me of my kids talking back to me. It’s always the final quip that sends me flying off the handle after many moments of perceived calm. Likewise, this muni portfolio was calm and collected until a 1.2% 10-year rate ballooned past 1.5%.

The good news for us muni investors is that the 10-year rate is due for a breather. As we discussed last week, we shouldn’t be surprised to see this yield revisit 1.1% or 1.2% in the near-term. That’s bullish for munis.

Looking ahead, however, we should prepare for a scenario where the 10-year rate rallies towards 2%. While that would not be the end of the world, it would pressure muni bond prices. Generally speaking, they rally when rates are falling, and they slide as rates rise.

So, let’s consider this careful approach:

- We should not be in a hurry to unload munis right now. If the 10-year rate takes the breather we are expecting, muni bonds (and funds) will benefit.

- However, we do need to keep an eye on 10-year yields. We may be adjusting our bond strategy in the months ahead.

If you’re looking for safe, monthly dividend payers (like these munis) to add to your retirement portfolio today, consider these 8%+ yields.

The recent rate spike has actually created a fantastic buying opportunity in these shares. As mentioned, each one of them does issue a dividend every 30 days. Plus, as I write, they are trading a bit below their intrinsic values (their NAVs).

This means their yields are elevated and they have some price upside to boot.

Deals like these—especially with monthly income payers—usually don’t last long. Please click here so that I can share the details with you.

Category: Dividend Yield