My 5 “Secret” Tips For Grabbing 8% Dividends, 79% Returns

Interest rates are (finally!) set to fall. As they do, we’re going to bag bargain-priced 8%+ dividends from a pattern we can set our watches to at times like this.

I’m talking about the mainstream crowd’s habit of “reaching for yield” when Powell & Co. drop rates, eroding yields on CDs, Treasuries and the like.

As these investors go on the hunt for higher payouts, I expect them to flock to closed-end funds (CEFs), one of our favorite income plays, thanks to the 8%+ yields these funds kick out.

But of course, we need to make sure we’re front-running the crowd into the right CEFs: those with high, safe, and ideally monthly payouts, while sidestepping the many dogs out there. We’ll do that with my 5 “ironclad” rules for CEF buying, which we’ll get into below.

How a “2019 Repeat” Will Hand Us Big CEF Dividends

First, to get a sense of the gains I see in store for CEFs in the next year, we need to start with the past, specifically the (seemingly innocent!) days of late 2018.

Back then, the Fed had just brought in its last hike of a cycle that started in late 2015. Then, starting in mid-2019, it made three rate cuts between then and the societal dumpster fire that hit in March 2020.

That’s the kind of downward drift we’re likely to see in rates in the coming months, whether this week’s cut is 25 basis points or 50—especially after last week’s CPI report, which showed inflation still moving lower, but the so-called “core” rate still ticking up just a bit more than expected month-over-month.

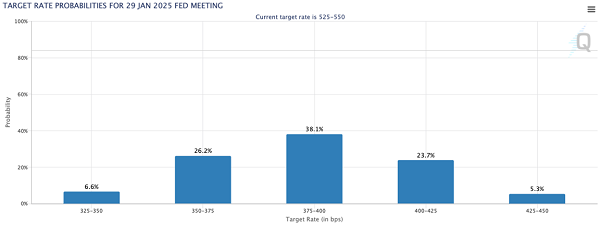

Of course, we’ll get the details on the Fed’s first rate cut when Powell and Co. drop their latest decision tomorrow. Futures markets, for their part, see rates down 125 basis points or so by the end of January, as of this writing:

That’s a slightly stronger downward move than we saw in 2019, but it’s in the neighborhood, so that time period is worth a look now.

How did CEFs do back then? Just fine!

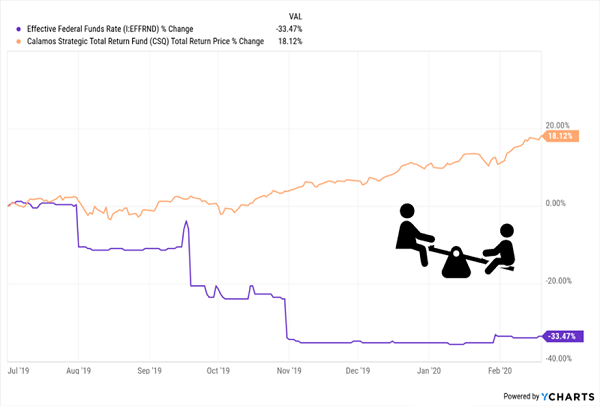

The Calamos Strategic Total Return Fund (CSQ)—a good benchmark for CEFs, since it holds two-thirds of its portfolio in stocks (in a sector breakdown similar to the S&P 500) and the rest in stocks and bonds—soared:

Our “Rates-Down, CEFs-Up” Pattern At Work

It makes sense: Most CEFs use leverage to bolster returns, and the resulting lower borrowing costs flow straight to their bottom lines (and to us through their rich 8%+ dividends!).

Meantime, with a hard landing looking less likely (as I discussed in my September 11 Contrarian Outlook article), continued strength of the US economy pushes up their share prices.

With that in mind, let’s roll through the five steps we need to take to unlock life-changing (and often monthly paid) dividends, as well as upside, from CEFs:

Step 1: Look Beyond “Price-Only” CEF Performance Charts

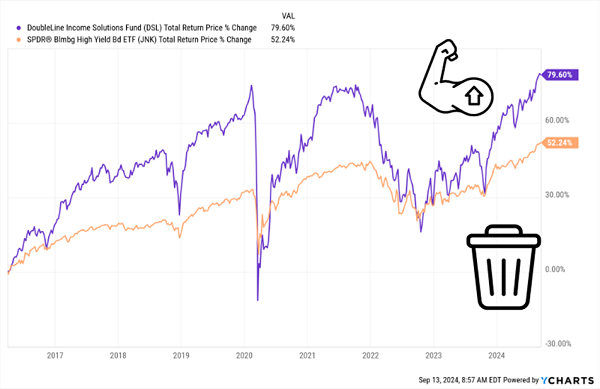

The DoubleLine Income Solutions Fund (DSL) has been a strong performer since we added it to our Contrarian Income Report portfolio back in April 2016. DSL yielded 11% when we bought, just a touch higher than the 10.2% current yield today.

And indeed, DSL has performed well for us, easily beating the corporate-bond benchmark SPDR Bloomberg High-Yield Bond Fund (JNK) and delivering an 80% return to date during our holding period, a strong performance from a bond fund.

DSL Junks JNK

Even so, traditional analysts have always missed the beauty of DSL and other CEFs because they only focus on price charts. But because CEFs throw off huge dividends, looking at price alone gives you at best half the picture, and sometimes much less than that!

DSL’s performance from its bottom during the COVID crash in March of 2020 until this writing illustrates the point perfectly:

As you can see above, the price action (in the third column) is a lot lower than the dividend-reinvested total return (in the fourth column) in this timeframe.

That’s not an indictment of CEF price performance, by the way. It simply shows that we need to look at CEFs—especially those with truly massive payouts like DSL—much differently than stocks and ETFs.

The bottom line: Take price-only CEF charts, which are the norm on screeners like Google Finance and Yahoo! Finance, with a grain of salt. Brokerage statements typically report price-only returns, too.

Step 2: Know What’s Funding Your Distributions

A closed-end fund can pay you from some combination of:

- Investment income,

- Capital gains, and/or

- Return of capital.

Of the three, investment income is preferable because it’s usually the most reliable. Many CEFs pay monthly distributions, so it’s best if they match up their payouts with steady income streams.

Capital gains from rising bond or stock prices can further boost distributions. But they are at risk of disappearing if the markets drop.

Finally, everyone assumes that return of capital is bad because it’s simply shipping your money back to you. But if the fund trades at a significant discount, this can actually be a savvy way to kick-start the closing of a discount window. More on this shortly.

Step 3: Collect Your Buy Price (and Then Some!) in CEF Dividends

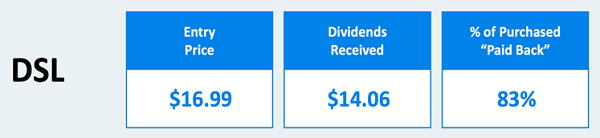

In a little more than eight years, we’ve collected 83% of our original purchase price in dividends from DSL, likely headed to 100%. Once you clear that level, everything else you pocket—in dividends and price upside—is gravy.

That’s what makes CEFs so compelling for retirement investing—when you buy CEFs with high, steady payouts, they act like an annuity, but better!

Step 4: View CEF Fees Differently Than “Bargain-Basement” ETF Fees

Most investors are conditioned to a fault by their experience with mutual funds and ETFs to search out the lowest fees. This makes sense for investment vehicles that are roughly going to perform in line with the broader market. Lowering your costs minimizes drag.

Usually, but not always. Closed-end funds are a different animal. On the whole, there are more dogs than gems. It’s critical to find a great manager with a solid track record. Great managers tend to be expensive, of course, but they’re well worth it.

The stated yields you see quoted, by the way, are always net of fees. Your account will never be debited for the fees from any fund you own. They are simply paid by the fund from its NAV. You receive the yield you see—a rare and happy case of truth in packaging!

Step 5: Demand a Discount

One aspect of the CEF structure lends itself perfectly to contrary-minded investing: a fixed pool of shares.

Mutual funds issue more shares whenever they want, fixed each day at NAV. But CEFs have a fixed share count, with their units trading like stocks. As a result, from time to time a fund will fall out of favor and find its shares trading at a discount to its NAV.

This is basically “free money” because these underlying assets are constantly marked to market (unlike mutual funds). If a CEF trades at a 10% discount, management could theoretically liquidate it and pay everyone $1.10 on the dollar. Or it can buy back its own shares to close the discount window (and boost the share price).

A discount is a great start, but context matters a lot here, since many funds have discounts that simply never change, so we want to make sure management has a plan to close it. Even better if that plan is backed by a discount that’s sharply narrowed, or swung to a premium, in the past, so we can “ride along” to price gains the next time it shrinks.

From the Publisher: 5 Monthly Paying CEFs Set to Pop as Rates Drop …

Kevin Wallen here. I’m the publisher of Contrarian Outlook.

I don’t normally break in on Brett’s editorial, but the CEF rules he just told you about are the perfect setup for 5 other CEFs we’ve got pegged to gap higher as rates drop.

These 5 funds come from our CEF expert, Michael Foster. They yield an incredible 10.5% today—and they pay dividends monthly too.

As rates drop, Michael sees these bargain-priced funds lined up to move higher. With an extra “assist” from their unusually wide discounts, 20%+ price gains could be on the table here, within the next year.

This post originally appeared at Contrarian Outlook.

Category: Dividend Stocks