15% Dividend Growth In A Shocking Industry

Double-digit dividend growth isn’t unheard of.

But it certainly isn’t common.

Do you want to know what’s really rare?

Increasing your dividend by 15% for 20 straight years.

It’s so rare only one company does it!

Williams-Sonoma (ticker: WSM) is a kitchenware and home furnishing retailer operating over 500 stores, primarily in the United States.

When you think about dividend growth, the retail industry probably isn’t the first to come to mind.

But what Williams-Sonoma has done is pretty remarkable.

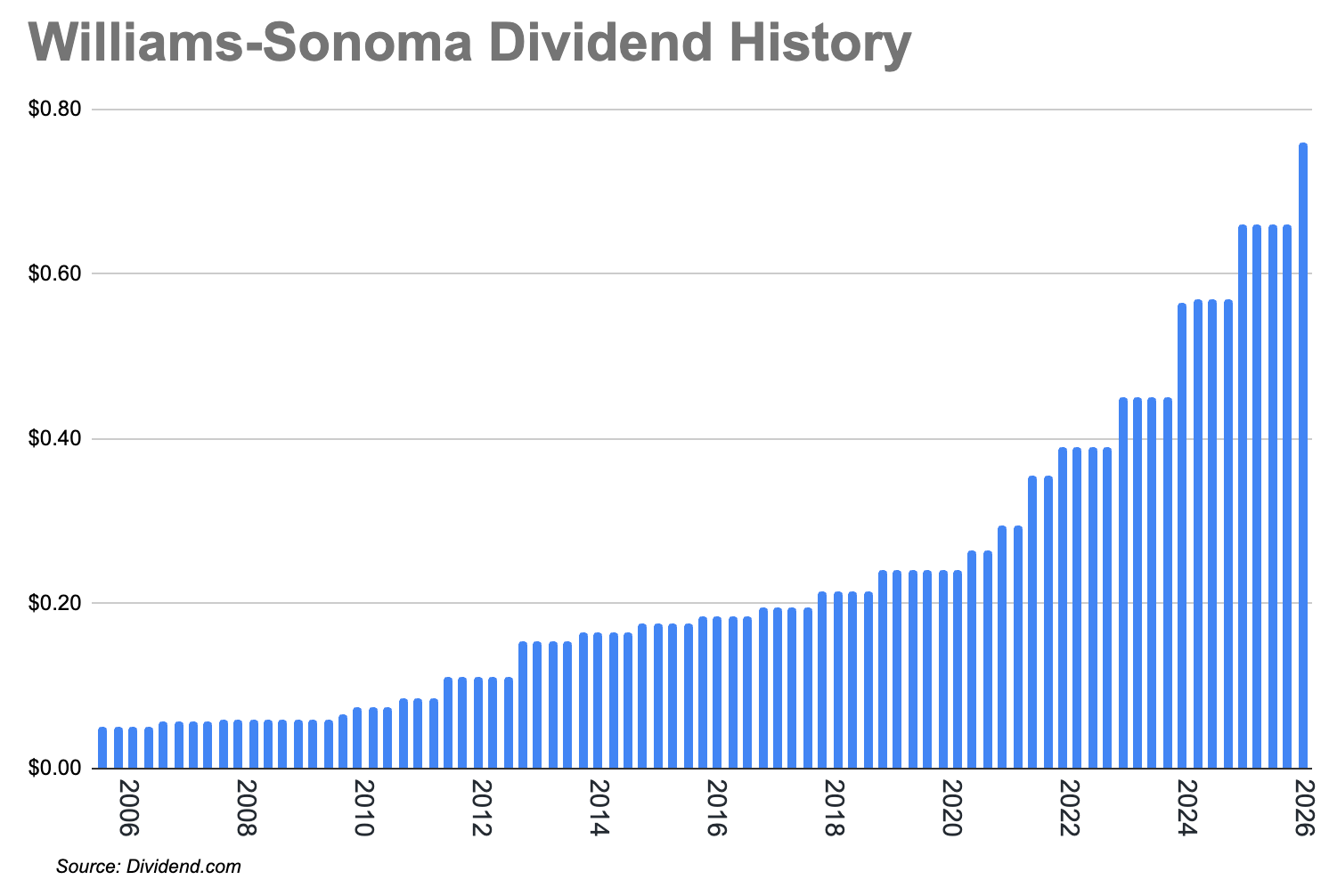

Just look at how fast it grew its dividend over the past 20 years.

Williams-Sonoma started paying a dividend in 2006 and has increased it every year since.

And the retailer just raised its dividend to $0.76 every quarter… but don’t wait too long.

You need to own stock in Williams-Sonoma by April 16 (Thursday) to get the higher payment.

I want to keep talking about dividend growth because it’s outstanding.

Williams-Sonoma’s dividend is doubling every 5 years.

The retailer was only making $0.30 payments back in 2021.

It’s important to keep the growth in mind when you see Williams-Sonoma’s 1.7% dividend yield.

The dividend yield is low and barely above the dividend yield for the S&P 500.

But if Williams-Sonoma keeps growing its dividend by 15% each year, your yield on cost will be over 3% in just 4 years.

Yield on cost measures the yield using your purchase price rather than the current stock price.

In 10 years, your yield on cost would be almost 7%!

Here’s the question though… Can Williams-Sonoma keep it up?

Williams-Sonoma is a cash machine.

Last year, the retailer made over $1 billion in free cash flow.

And Williams-Sonoma only used 30% of its free cash flow for dividend payments.

So the company has a lot of room to keep those dividends rising.

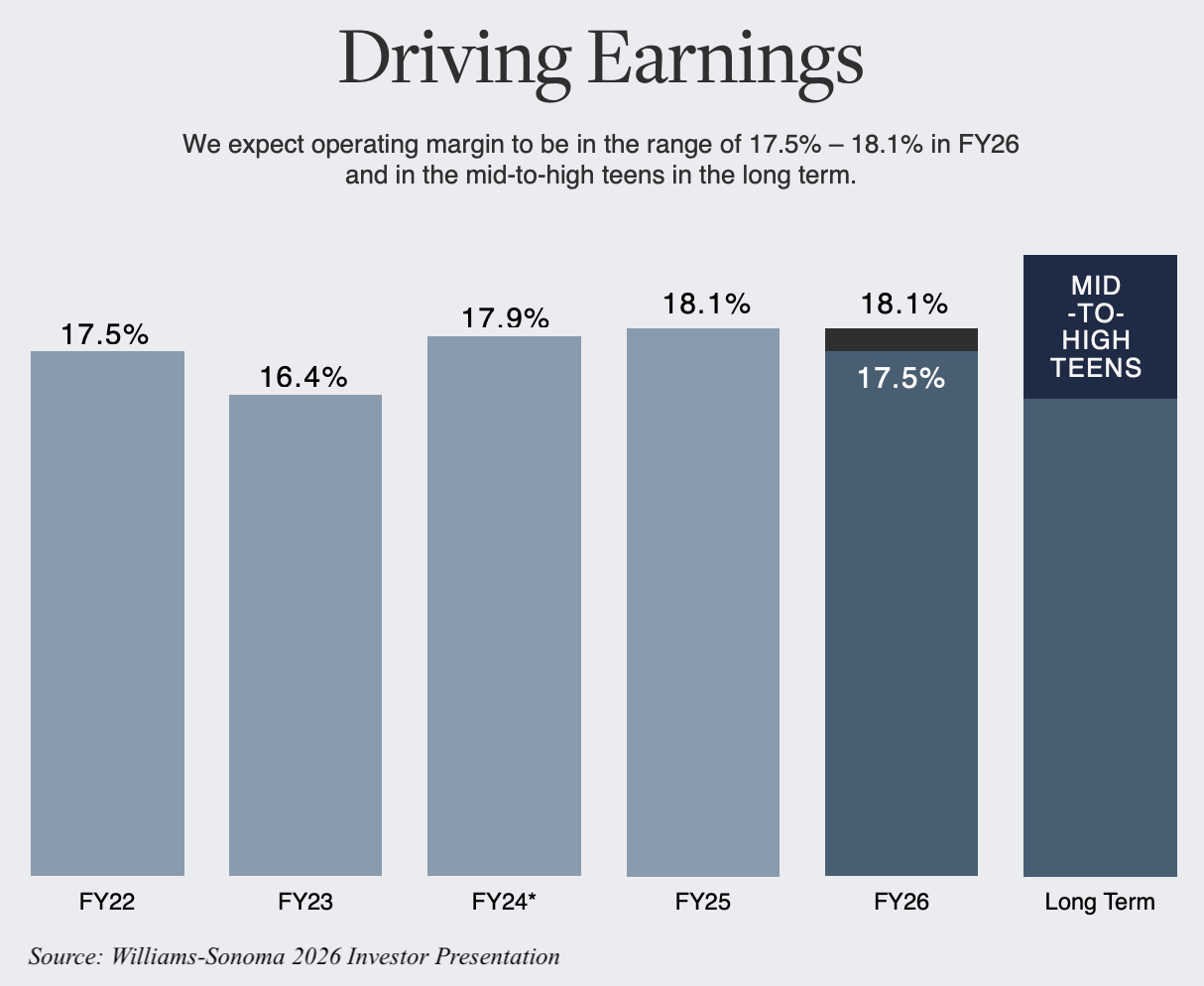

Plus, Williams-Sonoma is expecting earnings to continue to grow around 15% over the long-term.

So, Williams-Sonoma can keep its dividend payout ratio around 30% while still growing its dividend.

Why is Williams-Sonoma so optimistic about its future?

Williams-Sonoma is looking to expand outside of home furnishings and into professional spaces.

It’s a $2 billion opportunity for Williams-Sonoma, which could drive a 25% increase in the retailer’s revenue.

If the dividend and all of these opportunities don’t get you excited, Williams-Sonoma’s outstanding financials will.

Williams-Sonoma’s profit margin of 14% is one of the highest in the retail sector, and near an all-time high for the company.

And Williams-Sonoma’s 51% return on equity (ROE) is astounding.

If you’re looking for an incredible dividend growth company, Williams-Sonoma will be tough to beat!

What dividend stocks are you looking to buy right now?

Michael Jennings, Editor

Dividend Stocks Research

Category: Dividend Stocks To Buy?